Deployment of taxes has been front and centre as a tactic to calm Canadian housing market, but removing capital gains tax exemption on principal residences could turn market from hot to cold

What could the Canadian housing market look like in the next five years if governments consider further short-term taxation measures on homeowners as a way to cool things down? It could be a deal-breaker for buyers, says a new four-part report from RE/MAX Canada, developed in collaboration with CIBC and The Conference Board of Canada.

Unlocking the Future: The Economic Chapter offers a five-year outlook and analysis of how real estate in Canada might respond to specific scenarios through 2027, such as interest rate hikes, annual immigration volumes and taxation, and explores how these factors may impact Canadians’ capacity to buy, sell and maintain their homes in a stable manner. Subsequent chapters, which will be released throughout 2022, will consider the influence of climate change, the status of on-premise work, and technology on the Canada real estate market.

As the second quarter of 2022 approaches, many volatile factors are in play — from inflation to rising interest rates and a war in Europe — that will alter economic conditions in the short and long term. Based on specific plausible and confirmed scenarios, exploration within this report focuses on how policy decisions could affect real estate in Canada over the next five years.

Unlocking the Future: The Economic Chapter

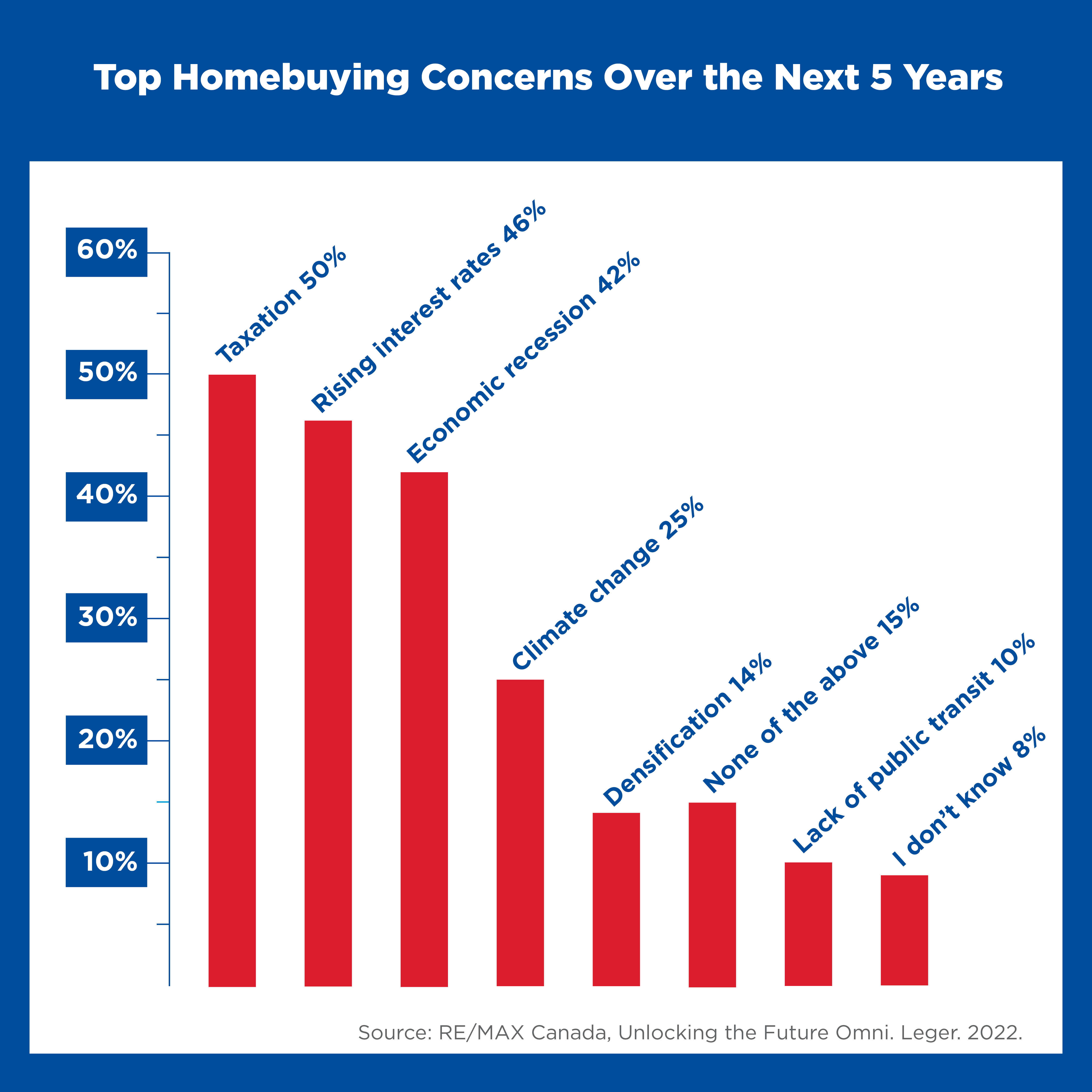

A recent survey, conducted by Leger on behalf of RE/MAX Canada, found that eight in 10 Canadians are asking themselves these same questions. Seventy-eight per cent of Canadians mentioned taxation, interest rates, economic recession, climate change, mixed housing, and/or public transportation as factors that cause them the most worry in their home-buying journey over the next five years.

In 2020, the Canadian economy experienced a 5.2-per-cent decline and in 2021 it saw 4.6-per-cent growth. As the economy rebounds from the pandemic, acute inflationary pressures are compelling central banks, including the Bank of Canada (BoC), to raise interest rates.

Additionally, the nascent conflict between Russia and Ukraine adds more uncertainty, impacting both inflation and economic growth.

According to CIBC Capital Markets, at the outset of the COVID-19 pandemic, three million Canadians lost their jobs and 2.5 million started working reduced hours. Now, the number of employed Canadians is above Canada’s pre-pandemic levels and Canada is exceeding its targets on the road to recovery (source). As Benjamin Tal, Deputy Chief Economist at CIBC Capital Markets, observed in developing this report, Canadians experienced the benefits of a recession, specifically ultra-low interest rates, during the first four waves of the pandemic without the costs of rampant unemployment.

In fact, according to Tal, Canada has a labour shortage, especially when it comes to trades – an area of employment critical to meeting the new housing starts our market demands. With the influx of immigration expected in the coming years and in particular, the federal government’s goal to welcome 432,000 immigrants in 2022, it is expected that demand in the housing market will increase, especially in urban centres such as Vancouver and Toronto, which are hot-spots for new Canadians. With rising demand, what solutions are on the horizon to address affordability? Can governments implement new tax measures, or are other scenarios more likely?

A majority of Canadians believe real estate is the best long-term investment.

“The Canadian housing market has historically given homeowners great long-term returns and solid financial security,” says Christopher Alexander, President, RE/MAX Canada. “In order to maintain this, as we look ahead, it’s crucial that governments and policy makers take a thoughtful and collaborative approach that addresses the worries Canadians have when it comes to home ownership.”

The survey commissioned by RE/MAX Canada also found that 61 per cent of Canadians believe real estate is the best long-term investment, and they do not expect this to change over the next five years. However, the majority of survey respondents do consider rising property-related taxes (64 per cent), rising interest rates (58 per cent), and possible capital gains tax (55 per cent), as barriers to buying a home in that timeframe.

“Despite the ongoing challenges facing Canada and the world, if economic decision-makers make pragmatic and evidenced-based decisions that do not penalize Canadians, but incentivize then with regards to interest rates, immigration and taxation, the housing market is likely to be stable, albeit expensive over the next five years,” continues Alexander.

Eliminating the capital gains tax exemption could deal a “blunt blow” to Canada’s real estate market.

SCENARIO: To manage ballooning deficits and calm a heated real estate market, the federal government removes the capital gains tax exemption on principal residences in the next five years.

“The deployment of ad-hoc taxes to lower the temperature on Canada’s housing prices, such as the foreign buyer’s tax, have been front and centre over the last few years; however, the potential of removing the exemption on capital gains for principal residences could truly disrupt the market,” says Jamie Golombek of CIBC Private Wealth.

Given the ballooning federal deficit sparked by the pandemic, speculation has increased that Ottawa could remove the capital gains tax exemption on primary residences. If this scenario was to transpire in the next 12 to 24 months, even in a modified or hybrid manner, it would upend the retirement plans of millions of Canadians who plan to cash in on the full gains from the sale of their principal home to fund

their retirement.

“The primary homes of Canadians represent the greatest store of value for most homeowners and removing a significant portion of that value by eliminating the exemption could cool the market in profound ways,” says Golombek. “While it theoretically will improve government coffers, it would be a blunt blow to the net worth of Canadian households, which in turn could dramatically swing the housing market from hot to cold.”

According to Golombek, most of the conversation over the last three to five years concerning the deployment of tax policy to cool the housing market has been focused on the Foreign Buyer’s Tax and taxes to curb speculation, such as the tax on the value of a vacant home (not considered a principal residence) imposed in British Columbia and Ontario. Yet, these measures impact a small segment of homeowners and have had little to no effect on real estate prices across the country.

Should this federal government, or another one, choose to apply a capital gains tax on the sale of a primary residence in the next five years, they could soften the blow to the market by making it prorated based on how long the property has been owned or based on the value of the home.

According to Golombek, if certain prorated caveats were introduced into the removal of the exemption, it could incentivize homeowners to put their properties on the market, dependent on the value of their home for retirement.

“Taxation in many ways, historically has stiffened our already existing supply issue by creating another barrier for sellers and buyers alike to consider when they buy or list their homes, says Christopher Alexander, President at RE/MAX Canada. “Punishing Canadians with a tax simply is not the solution. The focus should remain fundamentally on the supply challenges we are faced with in Canada as we look to the future and reducing barriers for Canadians.”

Golombek adds, “while a political ‘hot potato,’ a prorated capital gains tax on principal homes based on years of ownership could, in the short term, increase available inventory by motivating sellers to list, thereby creating a better balance between demand and supply and calming unprecedented year-over-year price hikes.”

Yet, removing considerable net worth from older Canadians in retirement or pre-retirement, will also negatively impact the transfer of wealth from this cohort to younger generations. If this were to unfold due to a new capital gains tax, then Canadians can anticipate less gifting to kids and grandkids (which again, represented one-third of new homebuyers in 2021), which in turn could further erode affordability.