Interest rate increases at a reasonable schedule of four times a year would create a stable and more relaxed environment for Canada real estate over the next five years

How might the affordability of real estate in Canada be impacted if interest rates continue to climb over the next five years? It could be good news, according to a new four-part report from RE/MAX Canada, developed in collaboration with CIBC and The Conference Board of Canada.

Unlocking the Future: The Economic Chapter offers a five-year outlook and analysis of how real estate in Canada might respond to specific scenarios through 2027, such as interest rate hikes, annual immigration volumes and taxation, and explores how these factors may impact Canadians’ capacity to buy, sell and maintain their homes in a stable manner. Subsequent chapters, which will be released throughout 2022, will consider the influence of climate change, the status of on-premise work, and technology on the Canada real estate market.

As the second quarter of 2022 approaches, many volatile factors are in play — from inflation to rising interest rates and a war in Europe — that will alter economic conditions in the short and long term. Based on specific plausible and confirmed scenarios, exploration within this report focuses on how policy decisions could affect real estate in Canada over the next five years.

Unlocking the Future: The Economic Chapter

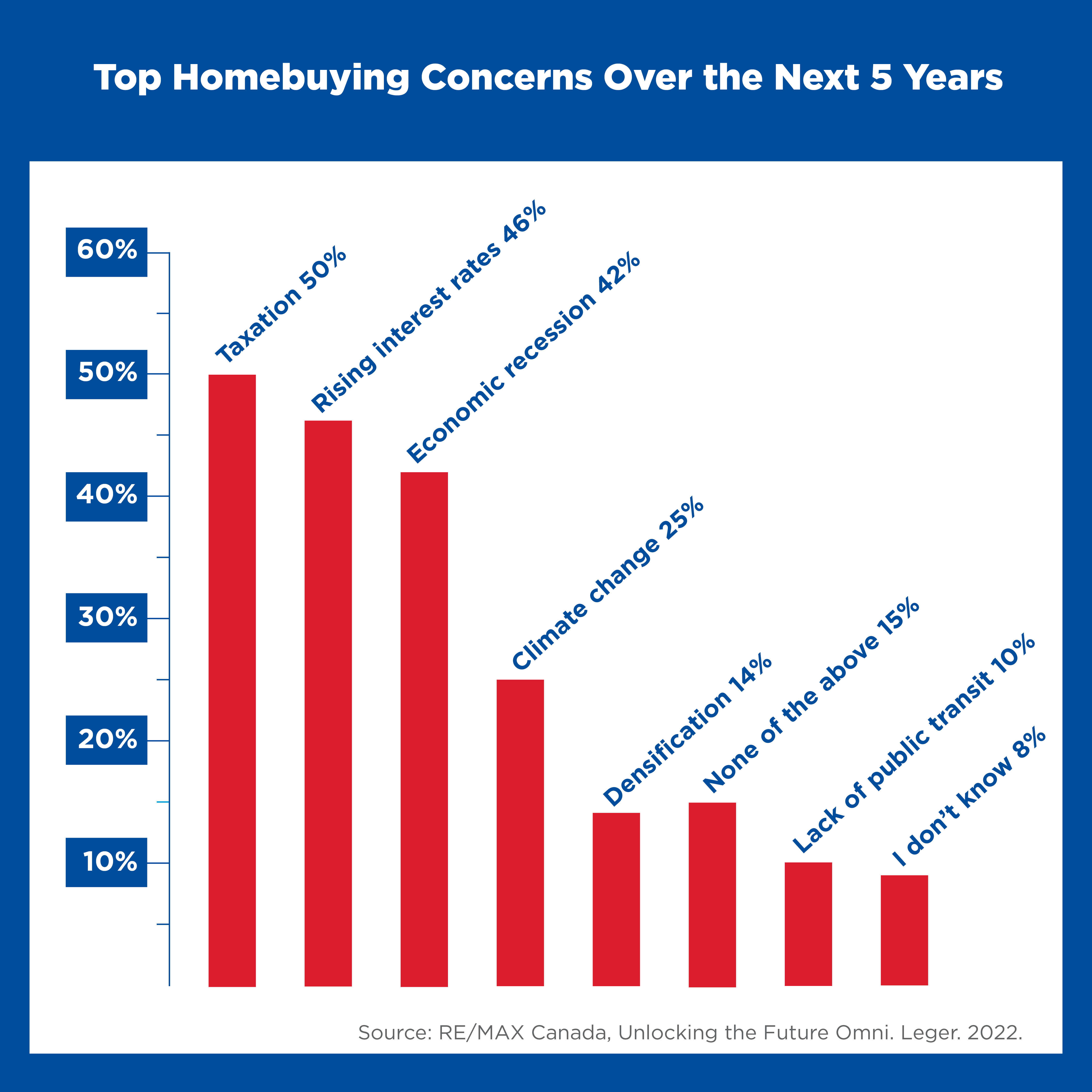

A recent survey, conducted by Leger on behalf of RE/MAX Canada, found that eight in 10 Canadians are asking themselves these same questions. Seventy-eight per cent of Canadians mentioned taxation, interest rates, economic recession, climate change, mixed housing, and/or public transportation as factors that cause them the most worry in their home-buying journey over the next five years.

In 2020, the Canadian economy experienced a 5.2-per-cent decline and in 2021 it saw 4.6-per-cent growth. As the economy rebounds from the pandemic, acute inflationary pressures are compelling central banks, including the Bank of Canada (BoC), to raise interest rates.

Additionally, the nascent conflict between Russia and Ukraine adds more uncertainty, impacting both inflation and economic growth.

According to CIBC Capital Markets, at the outset of the COVID-19 pandemic, three million Canadians lost their jobs and 2.5 million started working reduced hours. Now, the number of employed Canadians is above Canada’s pre-pandemic levels and Canada is exceeding its targets on the road to recovery (source). As Benjamin Tal, Deputy Chief Economist at CIBC Capital Markets, observed in developing this report, Canadians experienced the benefits of a recession, specifically ultra-low interest rates, during the first four waves of the pandemic without the costs of rampant unemployment.

In fact, according to Tal, Canada has a labour shortage, especially when it comes to trades – an area of employment critical to meeting the new housing starts our market demands. With the influx of immigration expected in the coming years and in particular, the federal government’s goal to welcome 432,000 immigrants in 2022, it is expected that demand in the housing market will increase, especially in urban centres such as Vancouver and Toronto, which are hot-spots for new Canadians. With rising demand, what solutions are on the horizon to address affordability? Can governments implement new tax measures, or are other scenarios more likely?

“The Canadian housing market has historically given homeowners great long-term returns and solid financial security,” says Christopher Alexander, President, RE/MAX Canada. “In order to maintain this, as we look ahead, it’s crucial that governments and policy makers take a thoughtful and collaborative approach that addresses the worries Canadians have when it comes to home ownership.”

The survey commissioned by RE/MAX Canada also found that 61 per cent of Canadians believe real estate is the best long-term investment, and they do not expect this to change over the next five years. However, the majority of survey respondents do consider rising property-related taxes (64 per cent), rising interest rates (58 per cent), and possible capital gains tax (55 per cent), as barriers to buying a home in that timeframe.(7)

“Despite the ongoing challenges facing Canada and the world, if economic decision-makers make pragmatic and evidenced-based decisions that do not penalize Canadians, but incentivize then with regards to interest rates, immigration and taxation, the housing market is likely to be stable, albeit expensive over the next five years,” continues Alexander.

The Impact of Rising Interest Rates on the Housing Market

SCENARIO 1: As the economy rebounds from the pandemic with strong employment and improved household savings, the BoC embarks on a steady cadence of four interest rate increases in the coming year.

“The enemy of the housing market is not high interest rates — that is good for the economy in fact. It is the pace at which those rates increase that is a big risk to housing,” says Tal. “Rate increases at a reasonable schedule of four times a year would create a stable and more relaxed housing market over the next five years.”

Tal anticipates inflation to ease in Q4 of this year. If inflation does not ease, the BoC is likely to respond by raising interest rates at a consistent quarterly pace to sustain a stable economy with healthy employment and a less-heated housing market.

Under these conditions, real estate in Canada, and especially in some of the largest cities, will remain expensive through to 2027, but not as heated on the pricing front as has been the case over the last two to three years. Moreover, interest rate hikes that do not overshoot a steady, pragmatic pace, should not unduly impact the ability of current homeowners to sustain the cost of their mortgages.

As Tal explains, “it’s important to note that given the five-year cycle of mortgages, those who are renewing now are in fact getting lower rates today than five years ago. Those existing homeowners who will be renewing in 2022 have a 150-basis point buffer, putting them in a very sustainable position.”

Tal’s one point of caution is to those who secured a mortgage in 2020 or 2021. Given they landed rates at historical lows, they are more exposed to higher rates, but even they should be able to sustain the added costs given the Stress Test, should the BoC sustain a steady cadence of rate hikes.

While demand for housing is likely to continue to outstrip supply, resulting in high prices, under a scenario like this with a higher interest rate environment, the housing market could be stable and less heated than what Canadians have experienced over the last five years.

“Canada’s housing market is far more stable than many people and industry watchers perceive,” says Tal. “Yes, there are specific caveats, such as prolonged inflationary pressure, that could upset the balance, but should the BoC stay pragmatic and consistent, the next five years look entirely sustainable for Canadians.”

According to CIBC Capital Markets, one-third of new homebuyers in 2021 were able to purchase due to financial support from family. This is double compared to what it was five years ago. Even move-up buyers experienced the impact of the generational wealth transfer, with 10 per cent buying a new home thanks to a gift.

The elusive historical transfer of wealth from the Boomers to Millennials and Gen Z is now in full motion. According to CIBC Capital Markets, one-third of new homebuyers in 2021 were able to purchase due to financial support from family. This is double compared to what it was five years ago. Even move-up buyers experienced the impact of the generational wealth transfer, with 10 per cent buying a new home thanks to a gift.

SCENARIO 2: As a result of prolonged inflationary pressure well above the BoC’s stated goal of 2.2 per cent, the BoC overcompensates with rate hikes, raising them more than six times annually.

Each recession Canada has experienced over the last 50 years has been triggered by central banks overshooting the ideal pace of interest rate hikes, according to Tal. In his assessment, this is the greatest potential threat to the stability of Canada’s housing market in the next five years.

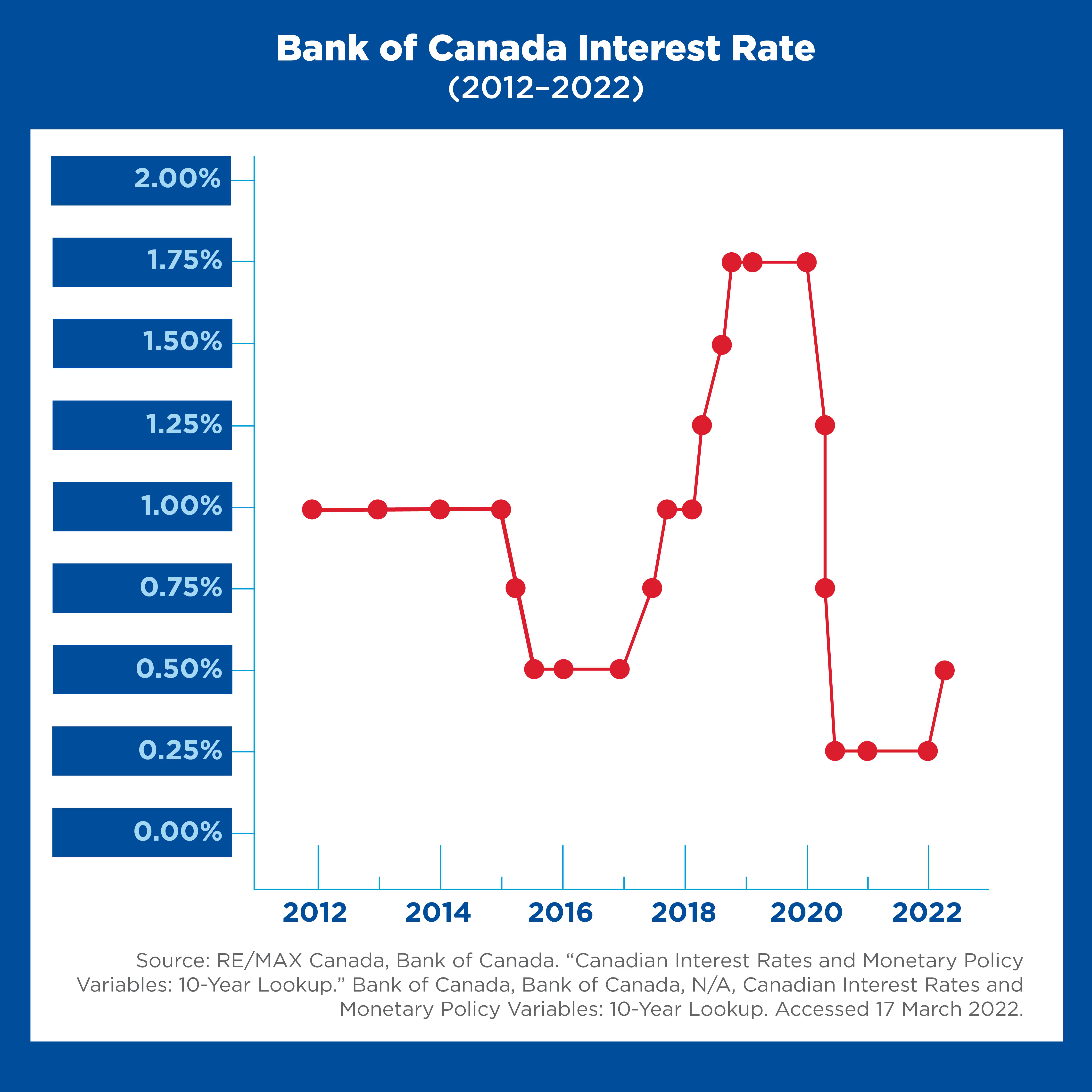

Canada’s inflation level currently sits at 5.7 per cent — the highest it’s been since 1991. With talk of interest rate hikes dominating the headlines, Canadians are understandably concerned about the impact of interest rates on housing and the economy. According to the Leger survey, 58 per cent of survey respondents believe that interest rates rising further will diminish their desire to buy or sell property in the next five years.10

Historic Interest Rates: The current BoC policy interest rate is 0.5 per cent, and the bank rate is 0.75 per cent. The last time interest rates rose above 0.5 per cent was to one per cent in 1967, 1968, 1974, 1979 and 1998, which resulted in a bank rate of six to 14 per cent on the high end in 1979.

“If we start to see interest rate increases twice per quarter or eight times a year to curb inflation, for example, then we could very likely fall into recession. This would obviously upend the economy, employment and housing,” says Tal. “Not only would demand fall significantly, but so too would the capacity of existing homeowners to sustain the borrowing costs of their homes.”

The other big caveat is COVID-19 and the potential for future waves caused by new variants; however, Tal perceives a recession precipitated the BoC as the primary threat to Canada’s economy and housing market.